BCIS infrastructure forecast: November 2018

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

19 November 2018

Civil engineering costs are forecast to rise 21% over the next five years (to 2Q2023); between 3% and 5% per annum. Increases over the final two years of the forecast are partially driven by sharper increases in wage awards due to labour shortages.

Civil engineering tender prices are forecast to rise faster than costs due to strong demand and increased pressure on site rates.

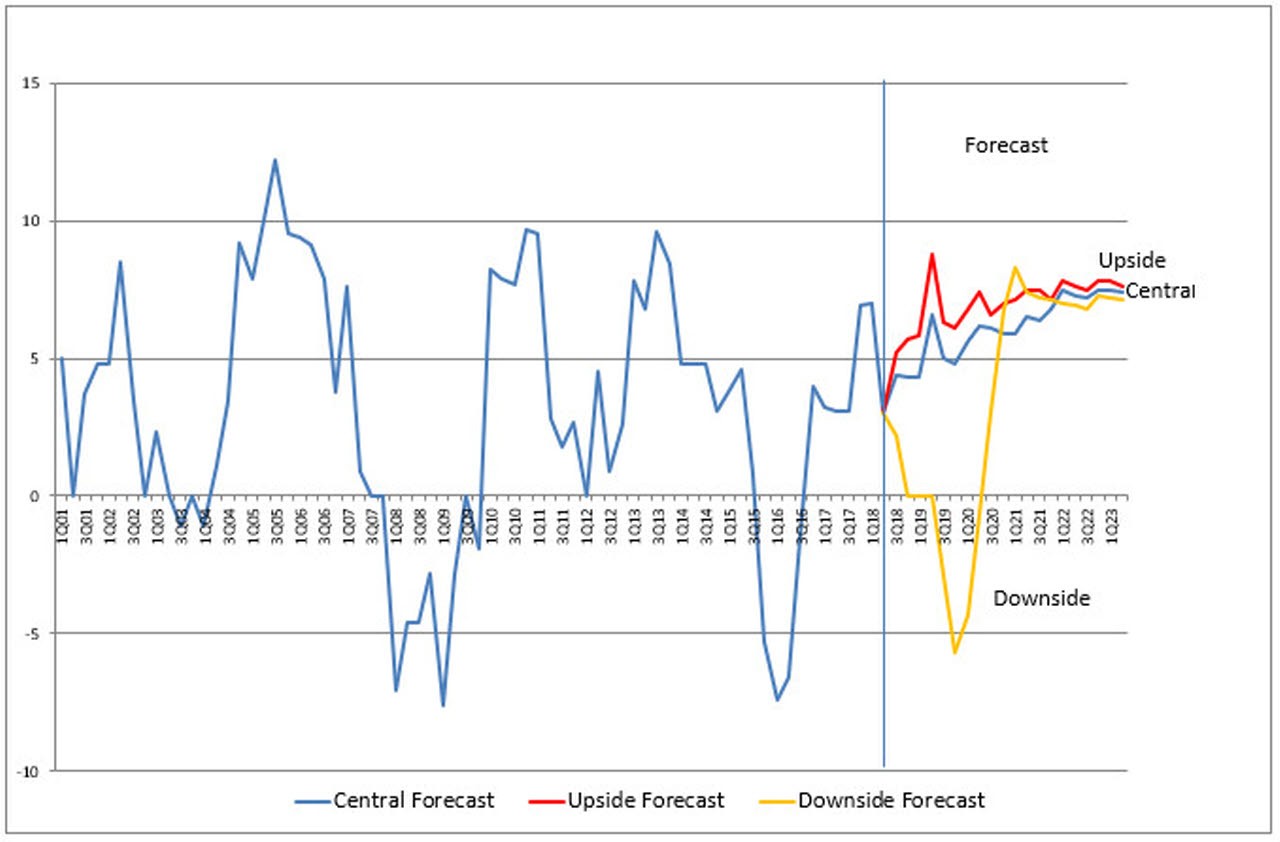

Tender prices are forecast to rise by 6% to 7% per annum. Over the forecast period tender prices, as measured by the BCIS Civil Engineering TPI (CETPI), will rise 39%.

Infrastructure construction output will rise by 52% over the forecast period.

The forecast is to be seen against a background of slowing Gross Domestic Product (GDP), with little signs of growth above 2% per annum over the forecast period.

Materials prices have been rising; prices for steel have risen sharply over the last year; oil prices have been very volatile. Wages have risen; nationally agreed wage awards increased in July 2018. Cost pressures are expected to continue.

There is potential for a turbulent ride for oil prices over the coming months, but currently BCIS has assumed that market forces will restrict significant upward movement above US$80, although prices might spike before falling back, depending on how reactive the market is.

The forecast is based on an orderly withdrawal from the EU when the agreed 'transitional period' ends on 31 December 2020. BCIS is assuming that there will be restrictions on the movement of labour after the end of the 'transitional period'. BCIS is assuming that this will impinge on the construction industry from around 1st quarter 2021, as the supply of new European labour dries up. This in turn will put upward pressure on promulgated wage awards as they try to keep pace with higher site rates obtained due to the reduced labour pool. Site rates over and above promulgated rates will be reflected in the market conditions factor, putting upward pressure on tender prices.

BCIS has also produced an ‘upside’ and ‘downside’ forecast based on the impact of different withdrawal agreements on construction output.

Although a 'No Deal' is currently being discussed as an option, this may encompass a raft of specific deals and has increased the range of possible outcomes. A specific forecast for this option has not been carried out. However, the likelihood is that a 'No Deal' would tend towards our downside scenario.

The forecasts are published in the RICS Infrastructure Information Service. For further information contact jmartin@rics.org.