RICS in Europe: Sustainable Real Estate Survey Europe 2025

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

04 March 2026

“We launched this survey to understand not just where the market stands on sustainability, but where it is heading. The results make it clear that Europe’s real estate sector is entering a new era: ESG expectations are reshaping the fundamentals of real estate. The question every professional must ask is simple: how future‑proof is this building?”

Edina Winkler MRICS; Associate, Valuation&Advisory, Cushman&Wakefield Hungary; Co-Chair of Valuation Working Group of RICS Hungary

Introduction

In fall 2025, we conducted a survey to better understand the European market’s current perception of green buildings, the evolving trends in occupier and investor demand, and the barriers that still hinder the adoption of Sustainability and ESG considerations in real estate decisions.

The survey collected 112 responses from valuers, developers, investors and other professionals across 30 countries, with most responses coming from Italy (25%), Germany (22%), Hungary (14%) and France (12%). The results offer an overview on how sustainability considerations are influencing real estate practices across Europe and where the sector is heading next.

In this article we combine the survey findings with broader market observations and industry trends to explore how ESG expectations are reshaping demand, value and risk across the built environment.

1. Growing Demand for Green and Sustainable Buildings

Sustainability dominated the decision making of both investors and occupiers in Europe last year. Survey responses show that two-third of the participants experienced significant or at least modest rise in demand for green buildings – an outstanding result compared to approximately 40% reported globally. Our Global RICS Sustainability report (2025) highlighted a slowdown in global demand growth, mainly due to declining interest across the Americas. This could be a response to changing political attitudes and policy focus. Demand growth across Europe has eased considerably over the last 12 months.

Strong demand for green buildings is unsurprising if these assets achieve higher prices. When asked if green buildings command a rental or price premium, responses supported this assumption:

- 72% of the respondents believe that green buildings achieve higher rents, with the largest share (32%) estimating a rent premium of up to 10% compared to non-green assets.

- 63% of respondents reported that higher sales prices are achievable, although a notable proportion (37%) still believe that market reflects a brown discount rather than a green premium. Responses varied: 31.5% indicated a price premium of up to 10%, and 25% reported a premium between 10% and 20%.

Together, these findings suggest that sustainability is no longer a niche preference, but a defining force reshaping Europe’s real estate markets.

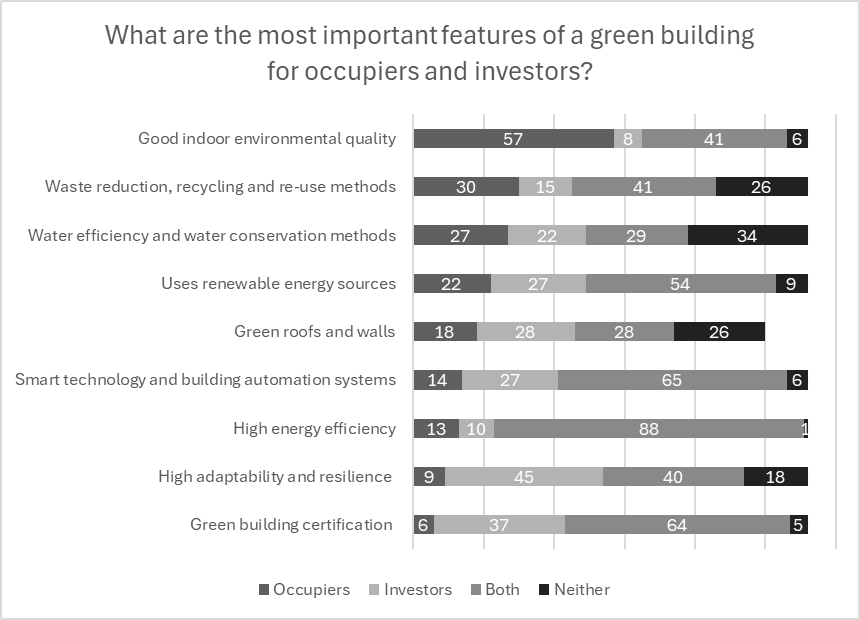

2. Features of Green Buildings: investors & occupiers

The regulatory environment continues to push both owners and users toward energy savings and more sustainable practices, which in turn is driving stronger compliance across the market. The survey confirms that both investors and occupiers prioritise high energy efficiency and recognise the importance of certifications such as BREEAM and LEED.

However, priorities diverge slightly when it comes to other building features:

- Occupiers rate indoor environmental quality as critical, and the availability of renewable energy sources is becoming an increasingly important consideration.

- Investors place greater emphasis on smart technologies and building automation systems, while also expecting high adaptability and resilience to climate related risks.

- Green roofs and walls, by contrast, were not regarded as a major priority by either group.

The findings align with our Global Sustainability Report and prevailing market sentiment: occupiers tend to favour high-quality buildings that meet green standards, primarily driven by reporting obligations and operational efficiency. Meanwhile, investors seek demonstrable sustainability credentials to mitigate long-term risks, such as future costs, regulatory exposure, and reputational damage from falling short of environmental expectations.

3. Investment considerations

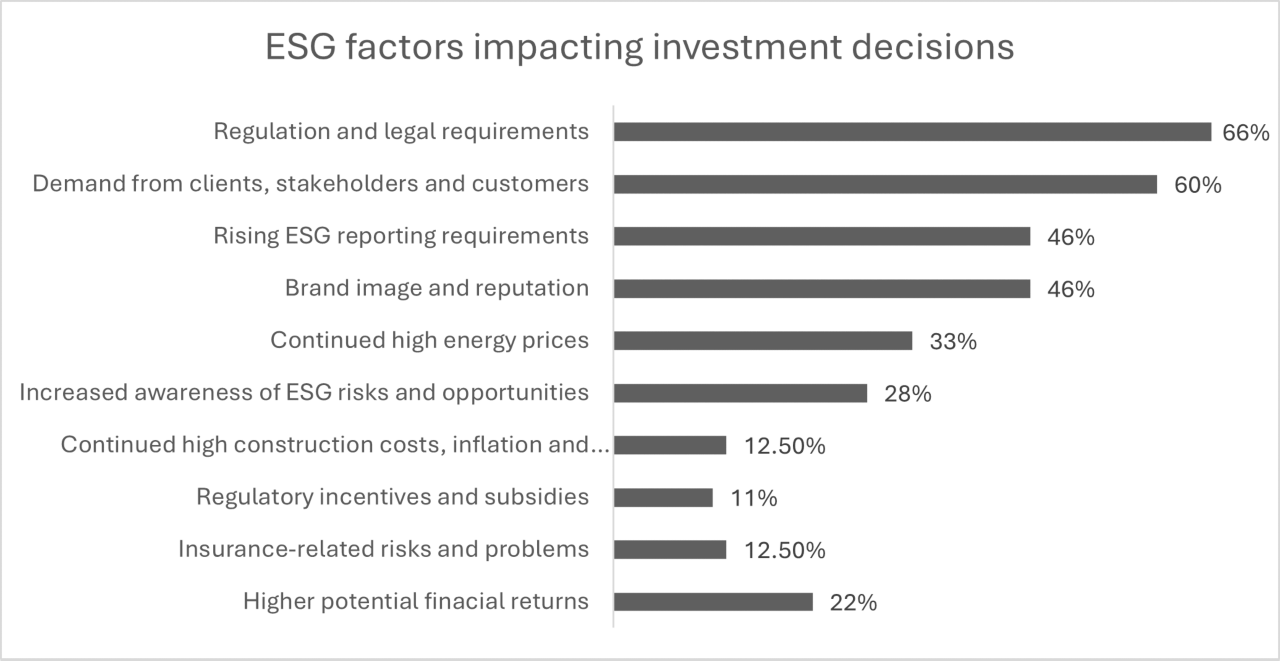

When asked which factors influence ESG decisions, respondents have identified regulation as leading driver with 66% underscoring the growing influence of compliance frameworks, followed by client and stakeholder demand at 60%, showing that investor preferences and stakeholder expectations are urging portfolio strategies to integrate ESG principles. "Rising ESG reporting requirements" and "Brand image and reputation" (both around 46%) also play significant roles, suggesting that transparency and public perception are increasingly critical in financial decision-making and in maintaining competitive advantage.

Policy is steering the sector towards carbon reductions globally. Europe is leading the way with the Energy Performance Building Directive (EPBD), Taxonomy and sustainability reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) and Sustainability-related Disclosure Regulation (SFDR). However, the current political shift has been impacting Europe as well, with most of the Sustainable Finance legislation undergoing major changes with the Omnibus proposals[1].

Interestingly, factors traditionally associated with financial performance — such as higher potential financial returns and financing incentives — rank much lower. This implies that ESG adoption is currently driven more by risk mitigation, regulatory alignment, and reputational management than by direct profit incentives.

This confirms that policy and compliance pressure are compelling investors to prioritize ESG criteria. As a result, property owners and managers are encouraged to ensure their buildings stay ahead of sector expectations: those who invest early in resilient, efficient, and future‑proof assets are likely to be best positioned in the evolving European market.

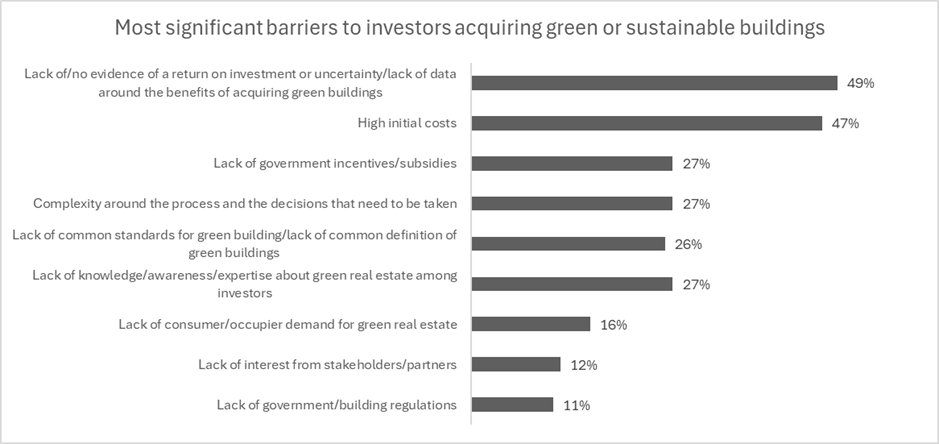

The survey results also show that the most significant barriers to investors acquiring green or sustainable buildings are financial uncertainty and cost‑related concerns (49%). Half of respondents identified the lack of evidence for a return on investment as the primary obstacle, closely followed by high initial costs (47%). These two factors dominate the landscape, suggesting that even though demand for green assets is rising, investors remain cautious when the financial upside is not clearly demonstrated. This hesitation is amplified by the perception that green investments may not yet offer predictable or comparable returns to traditional assets.

Beyond financial concerns, the data highlights a cluster of knowledge, regulatory, and process‑related barriers. Around a quarter of respondents pointed to issues such as lack of awareness, lack of common standards, complexity of the process, and insufficient government incentives. These responses indicate that the market still struggles with fragmentation and inconsistent frameworks, which can slow adoption even among willing investors.

Overall, the above suggests that ESG is evolving from a reactive obligation into a more opportunity‑oriented component of investment decision‑making.

4. Construction challenges

Interestingly, only a very small share of respondents reported supply‑side issues, reinforcing the view that the challenge is not the availability of green buildings. Respondents were also asked about the most pressing challenges faced in adopting sustainable construction practices. The dominant barrier is the high initial cost of sustainable construction, cited by 76% of respondents. Other major concerns include the high cost and low availability of sustainable materials (37.5%) and lack of evidence of benefits (35%). These indicate that upfront financial investment remains the most significant hurdle.

Lack of government incentives, inappropriate policies, and lengthy approval processes point to regulatory inefficiencies as well. The relatively low concern for green technologies may indicate that technological solutions exist but are underutilized due to other barriers. Overall, coordinated efforts across policy, education, and market incentives are needed to accelerate sustainable construction.

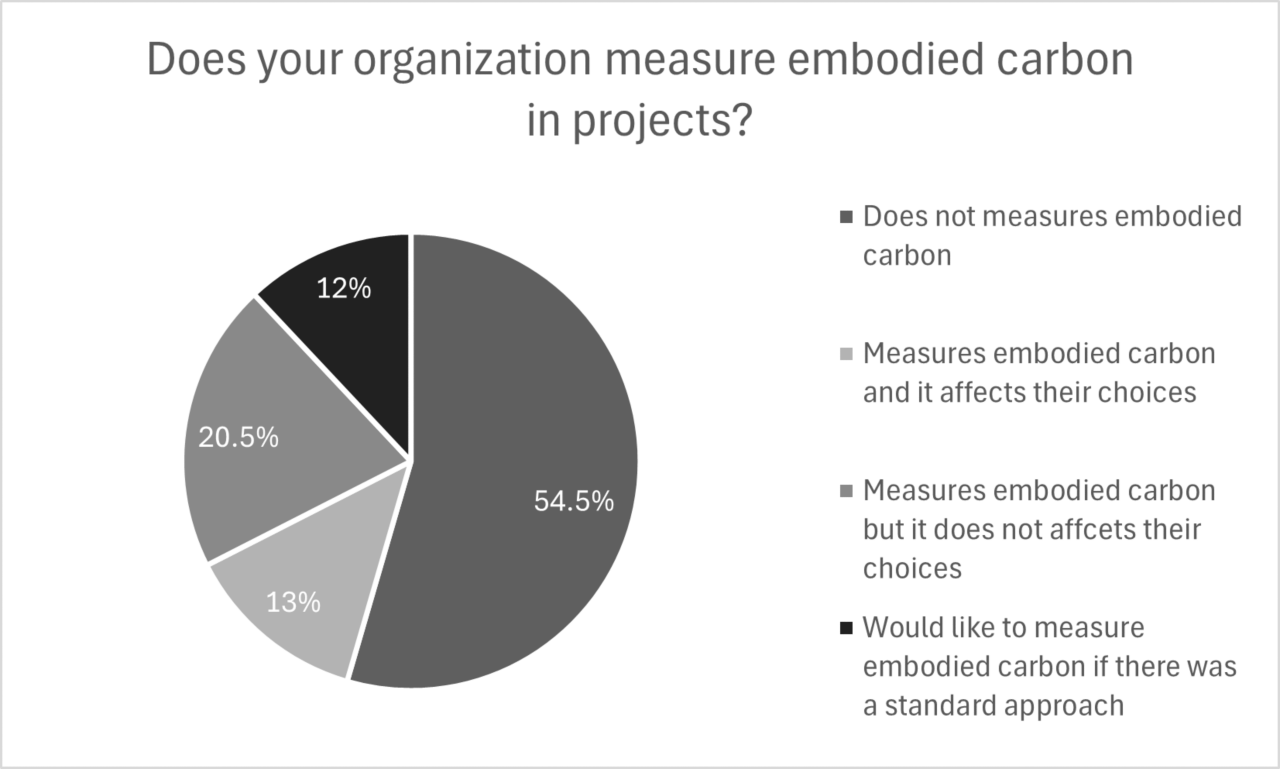

A lack of progress in measuring carbon emission was evident both in this survey and our latest Global Sustainability Report. 54.5% of respondents do not measure embodied carbon, and only 13% use such data to inform material and design choices. This indicates that while operational carbon reduction is well-established, embodied carbon remains an issue.

Respondents have identified the following changes related to embodied carbon:

- Standards to measure whole-life carbon too complex and requires competences and expertise not available in the market

- Stronger EU regulation is needed

The current edition of RICS Whole life carbon assessment (WLCA) for the built environment provides a global methodology for measuring whole life carbon emissions of new and existing built assets. This professional standard focuses on embodied carbon as well as operational and user carbon, providing a comprehensive and consistent approach for accurate carbon measurement and decision making.

A significant step has been made by EU, as under the EPBD, the life-cycle Global Warming Potential (GWP) will have to be calculated and disclosed in energy performance certificates for all new buildings with a floor area larger than 1,000 m² from 2028. This requirement will extend to all new buildings as of 2030. In December 2025, the Commission published new rules (C/2025/8723) outlining a common approach to calculating the life-cycle GWP of new buildings.

These rules create a common EU methodology to assess greenhouse gas emissions across a building’s full life cycle, it ensures comparability and consistency across EU countries, while leaving sufficient flexibility to EU countries.

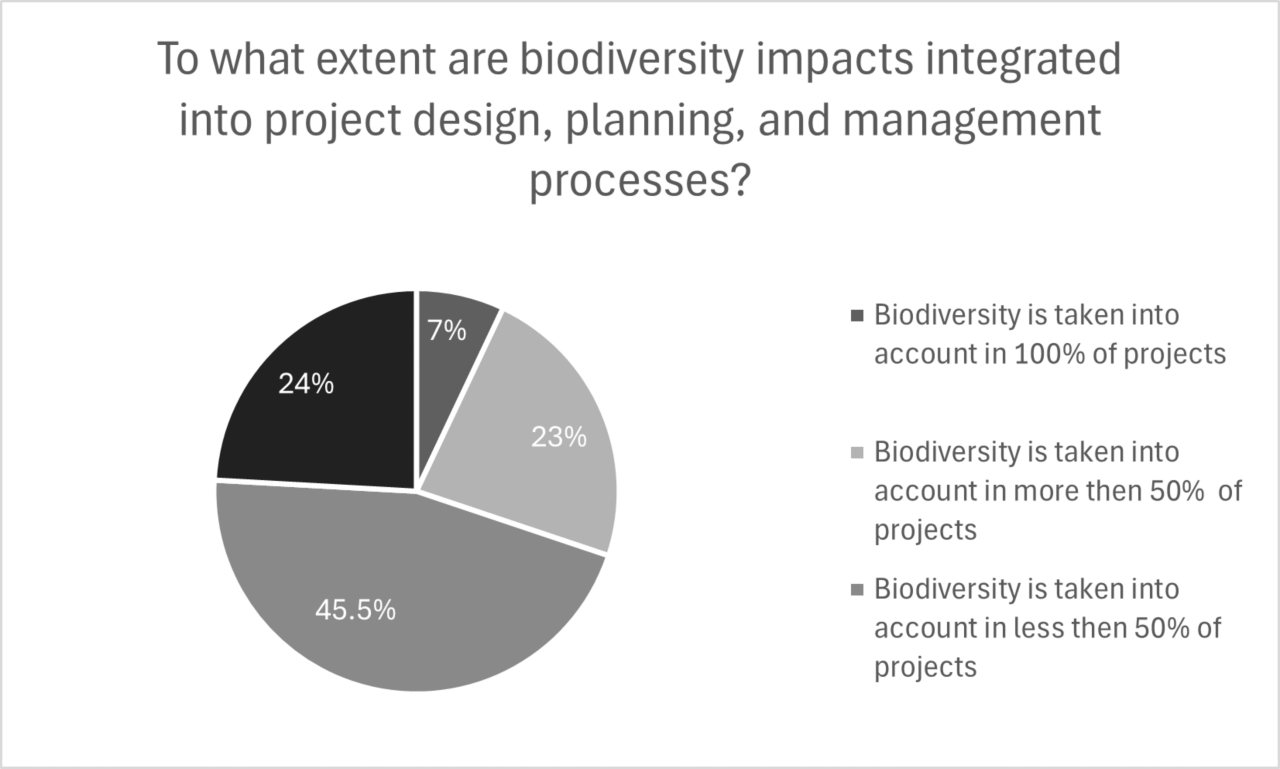

5. Biodiversity

In addition, we have asked participants to what extent is the impact is biodiversity in their projects. 45.5 % consider biodiversity in fewer than half of their projects, and only a small fraction have explicit biodiversity measurement frameworks in place. Respondents noted that biodiversity metrics remain “too vague” and “difficult to operationalize.

Similarly in our latest Global Sustainability Report, Europe has the lowest proportion of contributors who strongly agree on the issue of protecting biodiversity and the natural environment (19%).

6. Climate Resilience

A growing number of respondents reported that resilience to extreme weather and climate-related risks are becoming key concerns for investors, though these factors are not yet major considerations for occupiers.

There was broad agreement (75%) that adapting buildings to changing climate conditions and ensuring high energy efficiency and low operational carbon are now critical issues for built environment stakeholders.

However, our Global Sustainability Report, shows how assessments of adaptability and resilience are not yet common practices globally. With 8% of global respondents assessing adaptability and resilience to the effects of climate change in all projects.

RICS Guidance on ESG and Valuation

As ESG integration accelerates across Europe, professional guidance plays an essential role in helping valuers, investors, and other market participants make informed, resilient, and future‑aligned decisions. To support professionals navigating this evolving landscape, RICS provides a growing body of research, standards, and practical guidance aimed at integrating sustainability into valuation methodologies.

One of the key resources is The Future of Real Estate Valuations: The Impact of ESG, which explores how environmental and social performance indicators are influencing traditional valuation approaches. The publication outlines emerging global trends, investor expectations, and methodological challenges, offering valuers a forward‑looking framework for assessing ESG‑related risks and opportunities. It also highlights the importance of consistent terminology, data transparency, and sector‑wide collaboration—issues strongly echoed in the findings of our European sustainability survey.

Alongside the publication, RICS provides the The future of real estate valuations: The impact of ESG (Datalist), a practical tool designed to support valuers in systematically capturing and incorporating ESG‑related data into valuation reports. The Datalist summarises key ESG factors—such as energy performance, certifications, resilience indicators, climate‑related risks, etc. —and guides professionals on what information to request, record, and consider during inspections and analysis. The Datalist offers a structured starting point for standardising ESG inputs across asset types.

While the ESG Datalist outlines what ESG indicators matter, a harmonized ESG Questionnaire helps ensure valuers gather the right data from clients and property managers, aligning the practical data‑collection process with the recommended ESG indicators. The Hungarian Valuation Working Group has therefore initiated the ESG Questionnaire for Valuation as a national best practice, which is a structured template – available on the same RICS resource page - to help practitioners collect asset‑specific ESG information consistently at the outset of the valuation process.

In addition, RICS recently published an updated edition of ESG and sustainability in commercial property valuation, a practical guidance note designed to support valuers in embedding ESG factors within the valuation process. This edition reflects the latest regulatory developments, market practices, and sustainability reporting requirements, including the rapidly evolving EU policy environment. It aims to provide a structured approach to assessing sustainable building features, evaluating climate‑related risks, and interpreting evidence of green premiums or brown discounts—key themes highlighted by the survey respondents.

Together, these resources reinforce RICS’ commitment to advancing consistency, professionalism, and sustainability in valuation practices.

Conclusions

The findings paint a picture of a European real estate industry in transition, increasingly aware, progressively engaged, but still navigating complexity.

Demand for sustainable buildings is rising, driven by regulation and client expectations, supported by evidence of rental and price premiums. At the same time, financial uncertainty, high upfront costs, fragmented standards, and regulatory inefficiencies are slowing the pace of adoption, while unsustainable assets face growing risks of obsolescence.

Energy efficiency, green certifications, and smart technologies lead the list of investor and occupier priorities, while indoor environmental quality is paramount for end-users.

Embodied carbon and biodiversity measurement lag behind but represent critical next steps in achieving holistic ESG performance.

The findings suggest that the transition toward a more sustainable built environment is well underway, but unlocking its full potential will require clearer financial evidence, stronger policy support, and greater coordination across the industry. Ultimately, analytics, professional expertise, and cross-sector collaboration will be key to translating sustainability data into actionable insights, ensuring that green buildings are not just compliant, but genuinely resilient and value-enhancing.

Written by Edina Winkler MRICS, Associate Valuation & Advisory at Cushman & Wakefield Hungary and Valeria Sepe, Sustainability Specialist at RICS

Download

Published date: 25 February 2026