Building tender prices forecast

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

23 September 2019

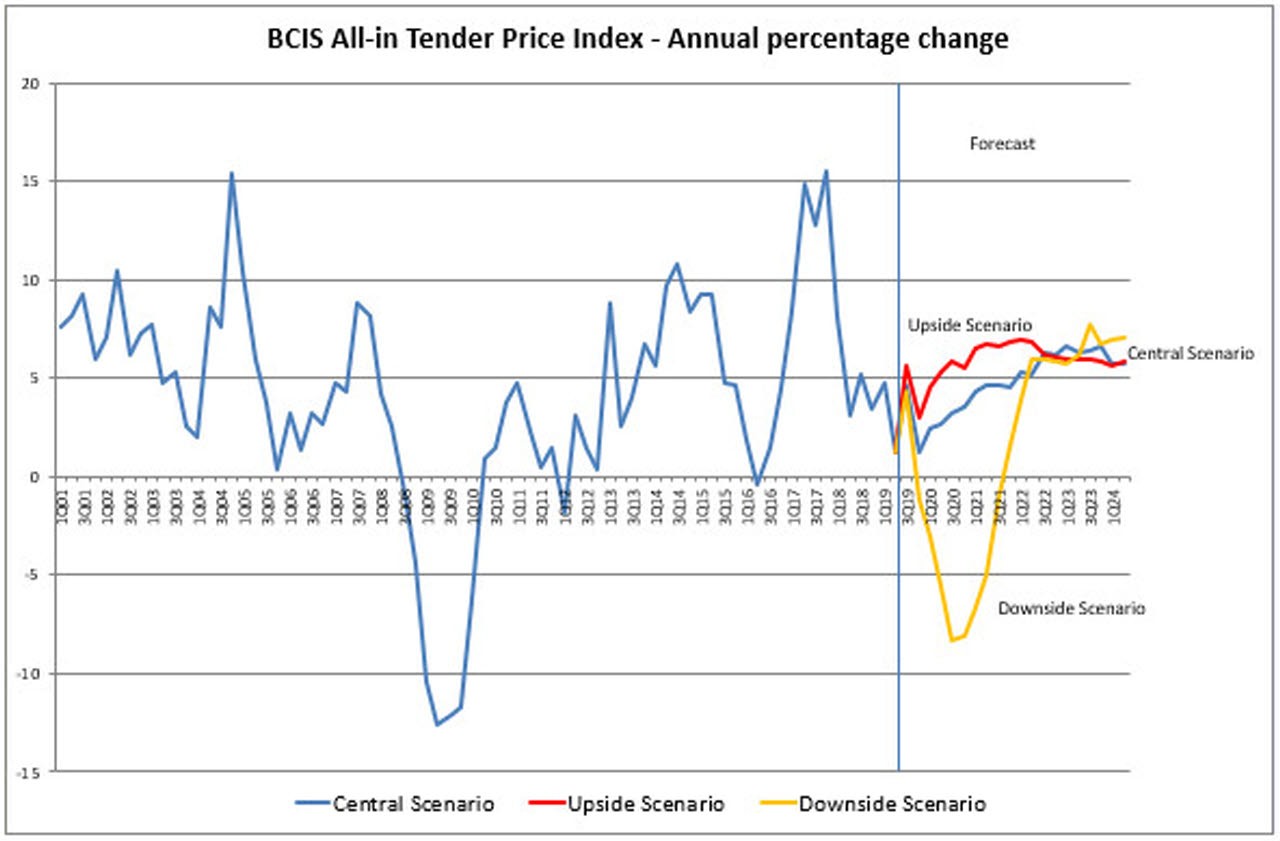

Over the next five years, building tender prices are expected to rise by 27%.

Tender prices are forecast to rise by 3% over the first year of the forecast period, by 5% over each of the following two years and by 6% per annum over the final two years of the forecast.

Building costs are forecast to rise by 20% over the forecast period, 3% over each of the first two years of the forecast period, 4% per annum over the following year, then by 5% and 4% respectively over the final two years of the forecast period.

Construction materials prices are expected to rise by between 3% and 4% per annum over the forecast period.

The average of wage awards is expected to be around 3% per annum over the first two years of the forecast period, rising by 5% over the following two years and by 4% over the final year of the forecast period.

BCIS Construction

Our construction data will help you to produce specific estimates for option appraisals, provide early cost advice and plan costs & benchmark

It is assumed that modest growth in new work output will ensue for 2019, with output picking up in 2020. Strong growth is expected over the following three years, driven primarily by very strong growth in the infrastructure sector, aided by growth in most of the remaining sectors, with a recovery expected in the private commercial sector from 2022. Over the five years 2019 to 2023, new work output is expected to rise by 21%.

There is still a great deal of uncertainty over the terms that will be agreed when the UK leaves the European Union.

While almost any outcome is still possible, BCIS will continue to produce forecasts based on three scenarios; these reflect the different outcomes from the exit negotiations from the EU and are equally likely. The uncertainty of the results of the Brexit negotiations will undoubtedly lead to BCIS revising its assumptions again as more is known.

In all scenarios, it is assumed that there will be no change of UK government over the forecast period, and that there is political stability in the rest of the world. A gradual rise in interest rates puts pressure on consumer spending.

A 'no deal' may encompass a raft of specific deals and has therefore increased the range of possible outcomes. A specific forecast for this option has not been carried out. However, the likelihood is that a 'no deal' would tend towards the downside scenario. Currently, a 'no deal' looks unlikely if the UK leaves Europe on 31 October 2019, but if the leave date is extended, 'no deal' could again be an option.